February 27, 2024

- Japan January CPI rises to 2.0% y/y (forecast 1.8%, December 2.3%)

- Risk of a partial US government shutdown March 1 is simmering.

- US dollar retreats modestly.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3493, overnight range 1.3484-1.3529, close 1.3506

USDCAD was uninspired but prices receded to broad-based, but minor US dollar selling in an overnight session, devoid of catalysts. Things didn’t change after the release of Durable Goods data for January, and the risk of a partial closure of the US government on March 1 may keep a damper on things.

Canada GDP is the next major piece of Canadian data, and it is released on Thursday. USDCAD could see some fresh selling pressure if GDP is stronger than expected, although the results could be overshadowed by developments in the US.

WTI oil prices are directionless in a $77.19-$77.95 band. Gains continue to stall due to ongoing fears that supply will exceed demand for 2024.

USDCAD Technicals

The intraday USDCAD technicals are slightly negative while trading below 1.3530 and looking for a retest of support in the 1.3440-60 area. A move below support suggests further losses to 1.3360 while a break above 1.3530 targets 1.3600.

The 100 day moving average at 1.3537 reinforces topside resistance while the 200 day moving average provides support at 1.3475.

For today, USDCAD support is at 1.3470 and 1.3440. Resistance is at 1.3530 and 1.3590. Today’s range is 1.3470-1.3540

Chart: USDCAD daily

Source: Daily FX

G-10 FX recap

It was another lackluster overnight session. Traders are keeping their powder dry ahead of upcpming US data and percolating fears about a partial US government shutdown on March 1. As usual, a core group of right-wing Republican politicians are at odds with many ultra-left-wing Democrats. And of course, there is the Trump effect. Europeans fear Trump partly because he is expected to throw Ukraine to the wolves (or Russia in this case), which would force the EU to step up their financial and military game.

Asian stock markets closed modestly higher. Australia’s ASX 200 gained 0.13% while Japan’s Nikkei 225 index was flat. European bourses are flat to slightly higher, while S&P 500 futures are unchanged.

US Durable Goods orders fell 6.1% in January which was worse than expected (forecast -0.45%) and December’s -0.3% dip. Durable Goods, ex-transportation were also weaker than expected (actual -0.3% vs forecast 0.2%). The US 10-year Treasury yield ticked up to 4.283% from 4.264%, following the news.

EURUSD is see-sawing in a 1.0842-1.0866 band. The US Durable Goods data helped put a floor under prices. Upside is still limited following yesterdays remarks by ECB President Christine Lagarde yesterday who said policymakers will need to see more evidence that the downtrend is sustainable before cutting rates.

GBPUSD is drifting in a 1.2671-1.2697 band. Traders are fixated on the upcoming UK budget as they are still haunted by former Chancellor Kwasi Kwarteng’s 2022 budget debacle.

USDJPY has a bearish bias inside a 150.12-150.71 range after January inflation was higher than expected. (CPI-ex-food actual 2.0%, forecast 1.8%, previous 2.3%). Analysts suggest that the data supports an April rate hike.

AUDUSD is trading negatively in a 0.6525-0.6550 band due to ongoing China economic growth concerns soft iron ore prices.

NZDUSD traded softer in a 0.6151-0.6176 range due to demand for AUDNZD ahead of the RBNZ meeting today (5:00 pm ET, 11:00 am Feb 28 Wellington time). The risk for NZDUSD is if the RBNZ stops talking about rate hike risks.

USDMXN is trading in a 17.0521-17.1185 range. Mexico’s trade balance dropped into deficit in January (actual $4.31 billion, forecast -$2.286 billion, December +$4.42 billion). USDMXN barely budged on the news.

The US economic calendar includes Case-Shiller Home Price Index (December forecast 6.0%, November 5.4%), and Consumer Confidence.

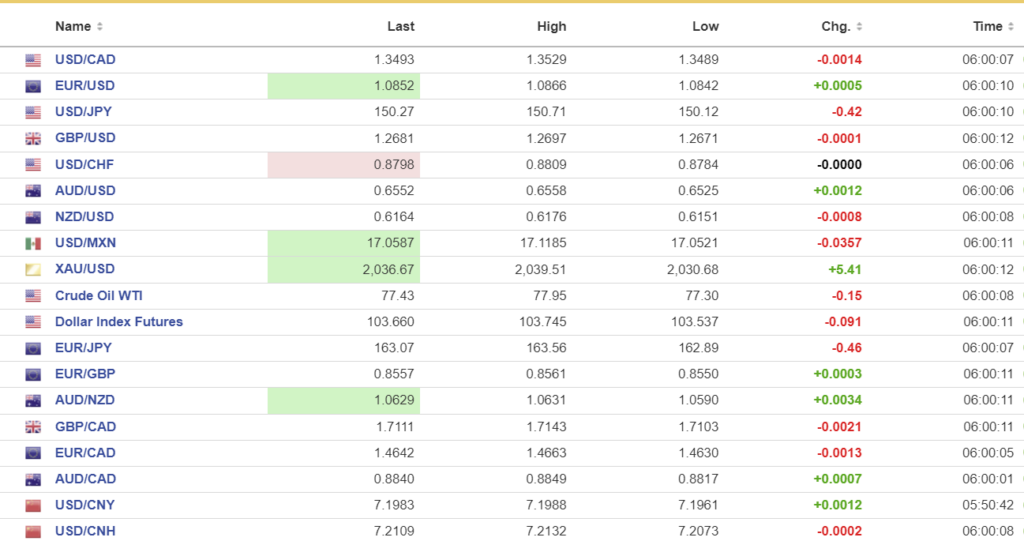

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: closed 7.1057, expected 7.1945, Monday 7.1080

Shanghai Shenzhen CSI 300 rose 1.20% to 3494.79.

UBS estimates that Chinese state-backed funds bought 57 billion of stocks on mail and exchanges this year.

Chart: USDCNY daily

Source: Bloomberg