April 24, 2024

- Canadian Retail Sales fall 0.1% in February 9 forecast 0.1%)

- German Ifo survey rises for third month in a row.

- US dollar opens with losses compared to yesterday, but a tad firmer form the close.

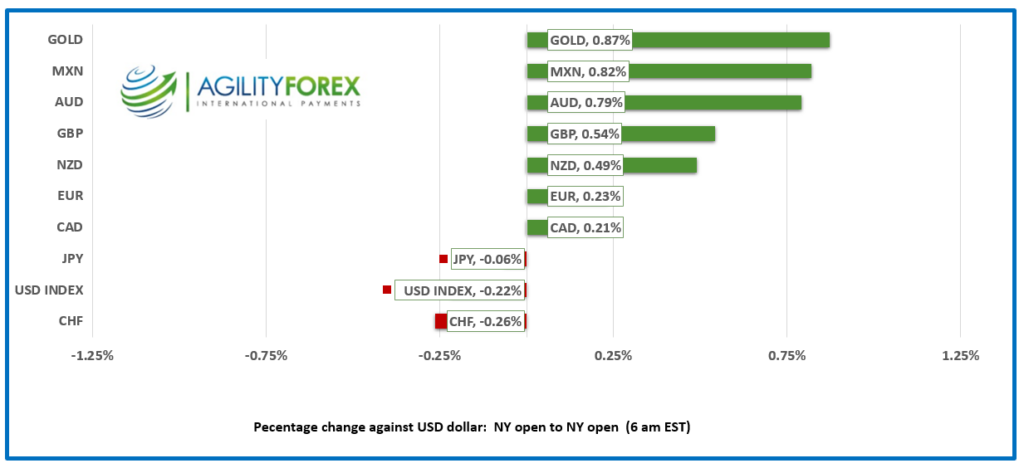

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3682, overnight range 1.3655-1.3708, close 1.3662

USDCAD dropped on the back of widespread US dollar weakness yesterday. The catalyst for the move was weaker than expected S&P Global PMI data, which helped fuel a rally on Wall Street. The moves is starting to be reversed, partly because it is the ISM PMI data that is perceived to be the better metric as it has a long-standing history, detailed sector-specific insights, and significant influence on monetary policy decisions.

Canada Retail Sales were lower than expected (actual -0.1% m/m vs forecast 0.1%) but tow-ticks better than in January. The data is stale but also reflects the weakness of the Canadian economy. The news combined with the US Durable Goods data, boosted USDCAD to 1.3708.

WTI oil has bounced between 80.84 and 83.58 this week and is currently trading at 82.74. The easing of Iran-Israel tensions has limited gains but hopes for increased demand has put a floor under prices.

USDCAD Technicals

The intraday USDCAD technicals are bullish while prices are trading above 1.3650 looking for a move above 1.3710 to extend gains to 1.3740. A move below 1.3640 targets 1.3540, while a break above 1.3710 will extend gains to 1.37.

The uptrend line from the beginning of January is intact above 1.3540.

For today, USDCAD support is at 1.3650 and 1.3620. Resistance is at 1.3710 and 1.3750. Today’s range is 1.3650-1.3720.

Chart: USDCAD 4 hour

Source: DailyFX

China and US are talking.

US Secretary of State Anthony Blinken is meeting Chinese officials who are a tad unhappy about the US providing $8 billion in aid to Taiwan, plans to ban TikTok, and proposed sanctions on Chinese banks for supporting Russia. China, in a not-so-subtle move, released a video showing the launch of a JL-2 ballistic missile from a nuclear submarine, and none of those missiles were made in North Korea.

Equity recap

Wall Street closed with gains and Tesla (TSLA-Nasdaq) is attempting to rally after announcing plans for a new, cheaper vehicle. Asia equity traders liked what they saw, and the major indexes closed with gains. Japan’s Nikkei 225 index rose 2.42% while a hot Australian inflation reading left the ASX 200 unchanged. European bourses are higher with the UK FTSE 100’s 0.51% rise, leading the pack. S&P 500 futures are barely in the green (0.06%). The US 10-year Treasury yield climbed from 4.598% at yesterday’s close to 4.64% in NY.

Durable Goods Prove Durable.

The US Census Bureau wrote “New orders for manufactured durable goods in March, up two consecutive months, increased $7.3 billion or 2.6 percent to $283.4 billion, the U.S. Census Bureau announced today. This followed a 0.7 percent February increase. Excluding transportation, new orders increased 0.2 percent. Excluding defense, new orders increased 2.3 percent.”

EURUSD

EURUSD is at the bottom of its 1.0678-1.0715 range despite the third monthly increase in the German Ifo index which rose to 89.4 from 87.9 in March. EURUSD continues to suffer from bearish technicals and ECB/Fed interest rate divergence. EURUSD is bearish below 1.0850, a level guarded by resistance at 1.0750 and the intraday downtrend line at 1.0730 which targets 1.0630.

GBPUSD

GBPUSD failed to hold on to yesterday’s gains and dropped from 1.2465 to 1.2422 and it is just above the low in early NY trading. Yesterday’s rally was fueled by comments from BoE Chief Economist Hu Pill saying that rate cuts were a ways off and that the risks were greater from cutting rates too early, than too late. The gains got an added boost by the US dollar slide following S&P global US PMI and Wall Street’s rally. Those gains are being eroded today. GBPUSD is bearish below 1.2470, looking for a retest of 1.2390.

USDJPY

USDJPY traded in a 154.74-155.17, range and broke above the 155.00 level in the wake of the US Durable Goods data. Traders seem to be daring the Finance Ministry and Bank of Japan to intervene. The BoJ policy meeting is Friday and there are reports that many policymakers do not believe that the weak yen is adding to inflation. The JGB-US 10 year yield spread has narrowed in the past month which is helping to cap USDJPY gains.

AUDUSD and NZDUSD

AUDUSD popped to 0.6530 from 0.6482 after quarterly inflation was hotter than expected. CPI rose 1.0% q/q (forecast 0.8% previous 0.6%) while RBA Trim mean (Core CPI rose 4.0% topping the 3.8% forecast. Money markets pared bets for rate cuts this year. The gains faded into NY.

NZDUSD traded in a 0.5930-0.5952 range. New Zealand’s trade deficit narrowed from -$12.06B to -$9.07B. Import and exports fell due to the weak economy stifling demand from consumers and businesses. ASB Bank believes that sticky services and core inflation will force the RBNZ to leave rates unchanged until 2025.

USDMXN

USDMXN traded defensively in a 16.9100-16.9945 range with price action tracking global risk sentiment and the weaker US dollar. Mexican first half-month inflation data showed a rise of 0.09% (forecast -0.3%, previous 0.27%). Core inflation was as expected at 0.16%.

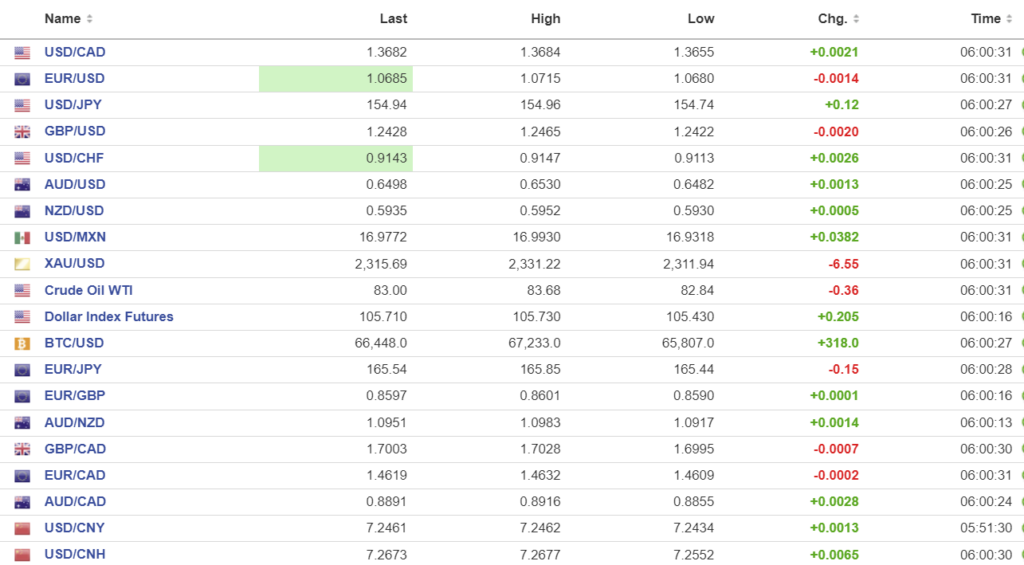

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1048 forecast 7.2336, (prev. 7.1059).

Shanghai Shenzhen CSI 300 rose 0.44% to 3521.62.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com