Photo:Bing Image Creator

August 30, 2023

- US ADP data rises less than expected.

- EURUSD supported by hawkish ECB outlook.

- USD opens lower compared to Tuesday with AUD outperforming.

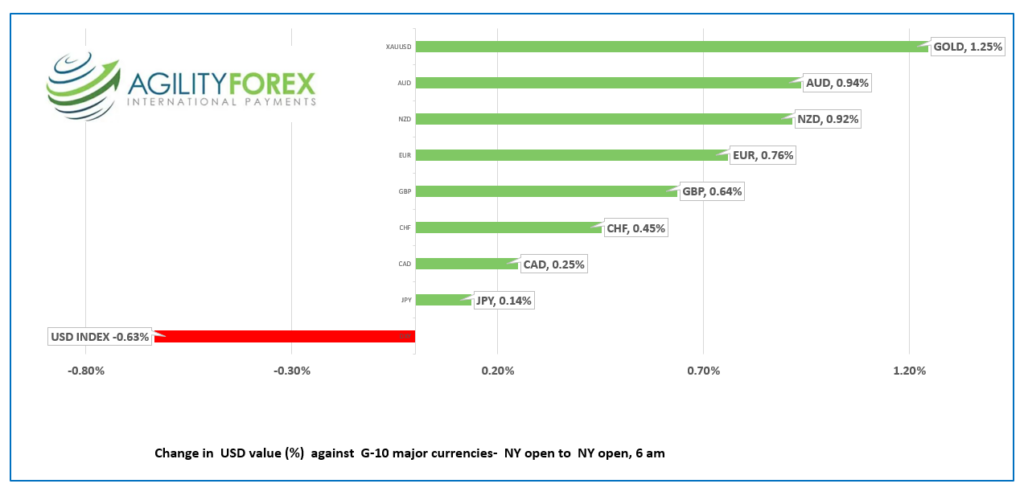

FX at a Glance

Source: IFXA/Raymond Peters

USDCAD Snapshot: open: 1.3563-67, overnight range: 1.3552-1.3578, close 1.3554

USDCAD bulls became steers yesterday, following the US Jolts and Consumer Confidence data which suggests the risk of higher US interest rates has fallen. USDCAD dropped from 1.3634 to 1.3553 yesterday, then nursed the wounds overnight.

Today’s lower than expected ADP data, alongside weaker than forecast US Q2 GDP weighed on USDCAD as it supports the idea that the Fed will cease raising interest rates. ADP Employment rose 177,000 (forecast 195,000, July 371,000) while Q2 GDP rose 2.0% compared to expectations for 2.2% growth.

WTI oil traded with a bit of a bid in a $81.17-$81.88 range supported by improving odds that the Fed will stop raising interest rates.

USDCAD Technicals

The intraday USDCAD technicals are mildly bearish while prices are below 1.3580 and looking for a break of the August uptrend line at 1.3550 to extend losses to 1.3480, which would also suggest that a short-term top is in place at 1.3650.

A move back above 1.3580, removes the downside threat and shifts the focus back to 1.3650.

For today, USDCAD support is at 1.3550 and 1.3510. Resistance is at 1.3590 and 1.3650. Today’s range 1.3520-1.3620

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

The winds of change are blowing. In Florida and the Carolinas, those winds come from Hurricane Idalia, which has been upgraded to a Category 4 storm. In FX and financial markets, the winds of change are blowing hawkish Fed forecasts away. Yesterday’s lower-than-expected JOLTS job openings data and weaker-than-expected Consumer Confidence index convinced some traders that the risk of further Fed rate hikes is diminishing. Equities rallied, the greenback dropped, and the US 10-year Treasury yield retreated to 4.116%.

The “Fed will pause” theme got a bit more juice after another series of weaker than expected US data this morning. ADP Employment rose 177,000 (forecast 195,000, July 371,000) while Q2 GDP rose 2.0% compared to expectations for 2.2% growth.

Asian equity traders appear to agree. Japan’s Nikkei rose 0.33%, while Australia’s ASX 200 gained 1.21%. Bank of Japan (BoJ) comments and Australian data probably played a much larger role in sparking the rally. European indexes opened mildly positive, then erased the gains, although the losses are marginal. The exception is the UK FTSE 100, which is up 0.30%. S&P 500 futures are unchanged.

EURUSD traded with a modest bid in a 1.0855-1.0908 range. Prices squeezed higher after German inflation was higher than expected in August (actual 6.1% y/y vs forecast 6.0%) but retreated from the peak as the result was still lower than July’s 6.2% result. Eurozone Economic Sentiment and Employment Expectations declined in August, which was largely ignored.

GBPUSD rallied following yesterday’s dovish US JOLTS job openings data and consolidated those gains in a 1.2619-1.2670 range overnight before popping to 1.2694 in the wake of the ADP data. UK housing market data showed further signs of slowing as mortgage approvals declined.

USDJPY rode a roller-coaster, rallying to 146.57, and dropping to 145.77 before climbing back to 146.30 in NY. The volatility was driven by weak Consumer Confidence data (actual 36.2 vs. forecast 37.5) and by comments from Bank of Japan officials. Board member Naoki Tamura said he felt achieving the BoJ’s inflation objective was clearly in sight and that he expected to see additional clarity in Q1 2024.

AUDUSD traded in a 0.6450-0.6483 range overnight following data that suggests the RBA may have completed its tightening cycle. July CPI rose 4.9%, compared to forecasts for a 5.2% increase and well below the 5.4% seen in June. Building Permits and Construction Work Done data were also lower than expected.

Top of Form

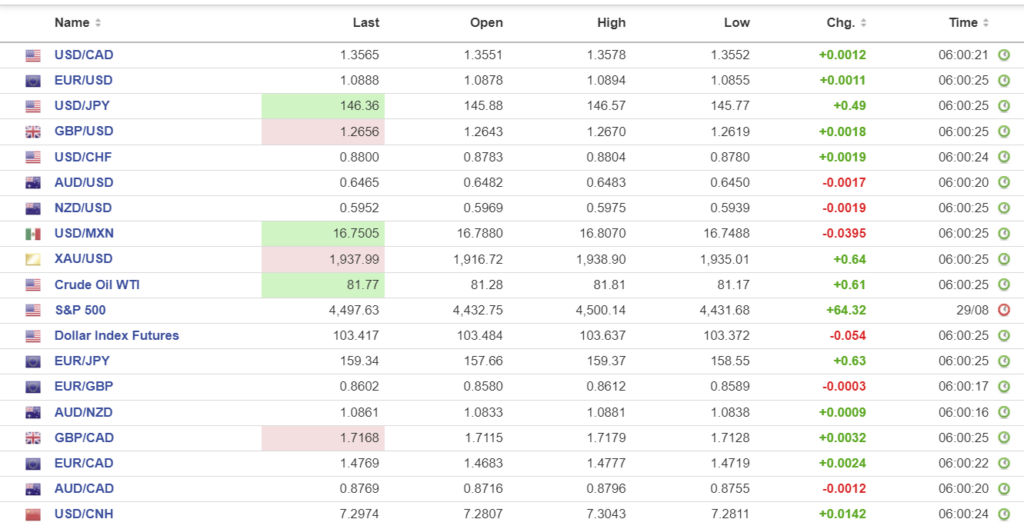

FX high, low, open

Source: Investing.com

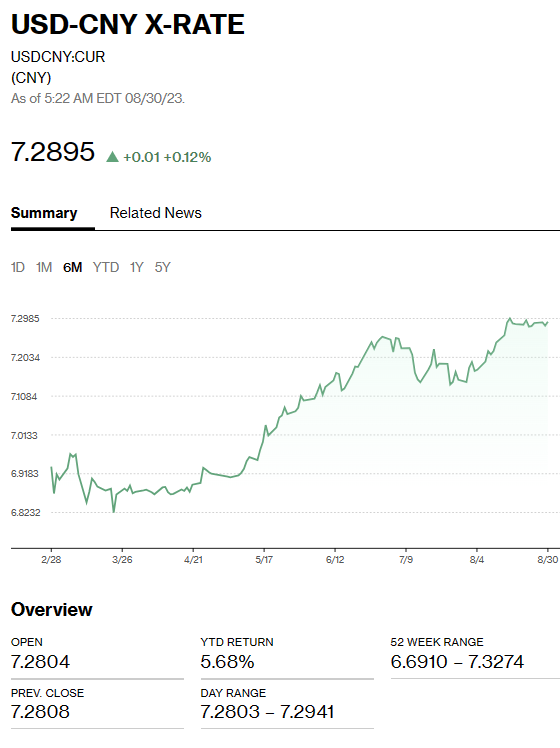

China Snapshot

Bank of China Fix: today 7.1816, expected 7.2773, previous 7.1851.

Shanghai Shenzhen CSI 300 fell 0.04% to 3788.51.

Chart: USDCNY 1 month

Source: Bloomberg